Cost Segregation Case Study

The best way to illustrate the direct financial benefits of a Cost Segregation Study is through the following KBKG case study:

What is a Cost Segregation Study & How Does it Work?

When a property is purchased, not only does it include a building structure, but it also includes all of its interior and exterior components. On average, 20% to 40% of those components fall into tax categories that can be written off much quicker than the building structure. A Cost Segregation study dissects the construction cost or purchase price of the property that would otherwise be depreciated over 27 ½ or 39 years. The primary goal of a Cost Segregation study is to identify all property-related costs that can be depreciated over 5, 7 and 15 years. For example, certain electrical outlets that are dedicated to equipment such as appliances or computers should be depreciated over 5 years.

KBKG goes beyond a traditional Cost Segregation study and will also separate all of the different building structural components (such as the roof, windows or HVAC units) so when they are replaced, a loss deduction can be claimed on them. For leased property, we also separate tenant leasehold improvements.

Cost Segregation of an Apartment Building Construction

A taxpayer completes a $5 million construction of an apartment building. $500,000 of the construction costs are initially identified by the taxpayer as furniture and equipment related (i.e. stoves, dishwashers and other appliances). The remaining $4.5 million of project costs are classified as building real property and depreciated over a 27.5-year class life by the taxpayer. The taxpayer appropriately decides to conduct a Cost Segregation Study in the tax year the project was completed and placed-into-service.

After the thorough analysis of the $4.5 million building real property by a Certified Cost Segregation Specialist, certain costs are identified as tangible personal property and land improvements. The results of the analysis are as follows:

- 17% of the $4.5 million identified as personal property (5-year depreciable class life)

- 8% of the $4.5 million identified as land improvements (15-year depreciable class life)

- 75% of the $4.5 million remains as structural real property (27.5-year depreciable class life)

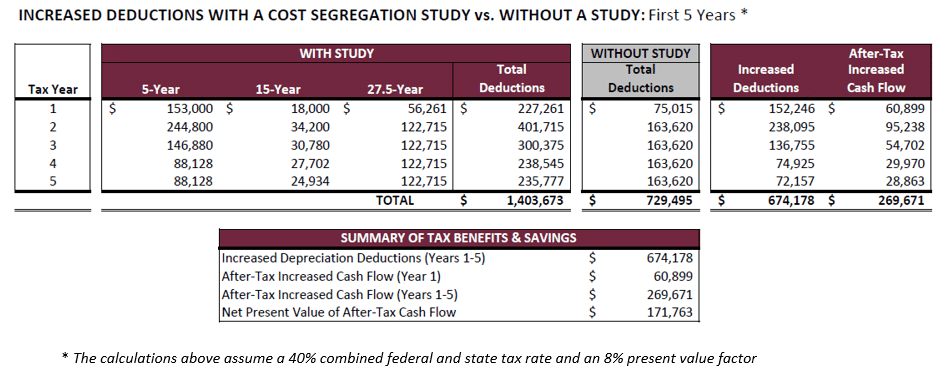

Tax Benefits & Present Value Savings as a Result of the Cost Segregation:

The following chart depicts the difference between total depreciation deductions of the apartment building for the first five years with and without a Cost Segregation Study:

Depending on when this building was placed in service, bonus depreciation rules may further accelerate the timing of these deductions.

The potential tax saving benefits derived from a Cost Segregation Study can be significant based on the cost basis of the project and type of property. Typically capital improvement projects larger than $500,000 or greater can benefit from cost segregation.

» Download the Cost Segregation present value savings analysis for an apartment building

Cost Segregation and Opportunity Zones: What Works and What Doesn’t Under the Latest Tax Law

Follow KBKG on Social Media Linkedin Facebook X-twitter Youtube By Eddie Price| Principal, Cost Segregation With the passage of the One Big Beautiful Bill Act (OBBBA), Opportunity Zones (OZ) have shifted from a temporary incentive to a permanent fixture, fundamentally altering how real estate investors should approach tax strategy. The bill creates new benefits specific … Read More

How Manufacturers Can Now Fully Expense Their Facilities and Real Property

Follow KBKG on Social Media Linkedin Facebook X-twitter Youtube By Lester Cook | Principal, Cost Segregation The 2025 One Big Beautiful Bill Act (OBBBA) introduced a significant opportunity for domestic manufacturers with the creation of Qualified Production Property (QPP) under new IRC §168(n). This new category allows eligible taxpayers to fully expense certain real estate … Read More

Real Estate Incentives Revitalized: What the OBBBA Means for Developers, Investors, and Owners

Follow KBKG on Social Media Linkedin Facebook X-twitter Youtube By Lester Cook | Principal, Cost Segregation The One Big Beautiful Bill Act (OBBBA), signed into law on July 4, 2025, permanently restores and enhances key provisions of the Tax Cuts and Jobs Act of 2017. From 100% bonus depreciation and qualified production property expensing to Opportunity … Read More

OBBB Tax Bill Makes 100% Bonus Depreciation Permanent – What You Need to Know

Follow KBKG on Social Media Linkedin Facebook X-twitter Youtube By Amar Patel | Principal, Cost Segregation Real estate investors know that tax strategies can make all the difference in maximizing profits. One of the most powerful, yet underutilized, tools available is the short-term rental (STR) loophole. This allows real estate investors to utilize property-related rental losses … Read More

Why You Should Only Use a Certified Cost Segregation Professional

Follow KBKG on Social Media Linkedin Facebook X-twitter Youtube When Cost Segregation studies are conducted, professional standards and technical accuracy are critically important, especially as studies are subject to IRS scrutiny. The best way to assess a provider’s qualifications is to confirm whether the person conducting your study is a Certified Cost Segregation Professional (CCSP) … Read More

Form 3115 for CPA’s: Unlocking Missed Tax Deductions Without Amending Returns

Follow KBKG on Social Media Linkedin Facebook X-twitter Youtube Many CPAs likely come across clients who have historically mis- or over-capitalized expenditures, particularly in real estate, retail or manufacturing. Fortunately, tax preparers don’t need to amend years of returns to correct these issues. The IRS offers a fix for this with Form 3115 (Application for … Read More

Navigating the Updated IRS Cost Segregation Audit Techniques Guide: What’s New?

Follow KBKG on Social Media Linkedin Facebook X-twitter Youtube By Amar Patel | Principal, Cost Segregation Cost Segregation remains one of the most powerful tax strategies for real estate investors, allowing them to accelerate depreciation and maximize deductions. On February 6, 2025, the IRS published the latest edition of the Cost Segregation Audit Techniques Guide (ATG), … Read More

How The Short-Term Rental Loophole & Cost Segregation Can Benefit Passive Investors

Follow KBKG on Social Media Linkedin Facebook X-twitter Youtube By Amar Patel | Principal, Cost Segregation Real estate investors know that tax strategies can make all the difference in maximizing profits. One of the most powerful, yet underutilized, tools available is the short-term rental (STR) loophole. This allows real estate investors to utilize property-related rental losses … Read More

The Interplay Between Cost Segregation and a 1031 Exchange

When a property is acquired in a Section 1031 like-kind exchange, tax preparers should consider several facts before deciding how to best depreciate the carryover basis from a relinquished property. When a cost segregation study is also considered on the newly acquired property, additional analysis is recommended before finalizing the 1031 tax basis calculations. To … Read More

100% Bonus Depreciation Making a Comeback?

By Amar Patel | Principal, Cost Segregation In a speech to a joint session of Congress, President Trump outlined priority tax legislation expected later this year to restore provisions of the Tax Cuts and Jobs Act (“TCJA”), which includes “providing 100% expensing, retroactive to January 20, 2025”. This leads many to believe that 100% Bonus Depreciation … Read More