As featured in Accounting Today

Real estate owners have limited options to pull cash out of a 1031 exchange without having to pay income tax. With proper tax planning, this problem can be solved with a cost segregation study. The application of cost segregation for this purpose may vary depending on the tax rules in place at the time of exchange. In this article, we will examine how to pull tax free cash out of a 1031 exchange with bonus depreciation in place and when bonus depreciation is phased out.

1031 Considerations

Cash received in a 1031 exchange that is not used to purchase a replacement property is referred to as “boot” and these funds are generally taxable. Since properties that are exchanged are usually not equal in value, cash or non-like-kind property may be transferred or received to even up both sides of the exchange. When boot is received in a qualifying like-kind exchange, gain is recognized up to the amount of boot received (“partial gain recognition”). The amount of boot is measured by the money or fair market value of non-like-kind property received.

Cost Segregation

A Cost Segregation Study is a tax planning tool based on the principles of engineering that allocates components of a building’s depreciable tax basis, which are generally depreciated over 39 or 27.5 years, into the appropriate asset classifications which can be depreciated over shorter tax lives (5, 7, 10 or 15 years) for federal and state income tax purposes.

Bonus Depreciation

Bonus deprecation allows for an accelerated first-year deduction on property that is typically depreciated with a tax life of less than 20 years. Through the end of 2022, qualified property is subject to a bonus depreciation rate of 100%, which means 100% of the asset’s basis is deducted in the first year. Bonus depreciation rates phase down to 80% in 2023, 60% in 2024, 40%, in 2025, and 20% in 2026.

How Cost Segregation allows for tax-free cash

Scenario #1. Inside the Bonus Depreciation Window: With bonus depreciation in place, a cost segregation study can be performed on either the relinquished property or replacement property to generate enough first-year deductions to offset taxable income generated from receiving boot.

For example, in 2022 Taxpayer A sold a property that was acquired in 2018, which had a Tax basis of $1,900,000, in a 1031 exchange for $3,000,000 + $350,000 of cash. The recognition of cash “boot” triggers a taxable event for Taxpayer A.

As a result of the transaction the realized gain is $1,450,000 of which $350,000 is recognized gain (Taxable) and $1,100,00 is deferred gain (Non-Taxable). The total tax due is $129,500 ($350,000 x 37% tax rate)

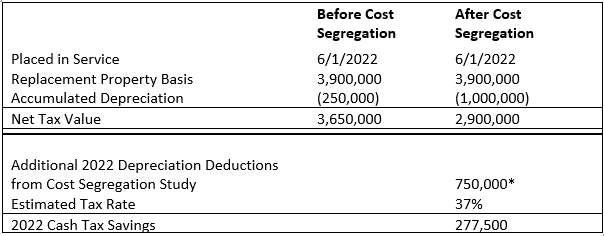

Taxpayer A utilized the 1031 proceeds to acquire a replacement property for $5,000,000. The basis of the replacement property must be reduced by the deferred gain of $1,100,000 leaving total basis in the replacement property of $3,900,000. The example below highlights how a cost segregation on this replacement property can be utilized to offset the tax due because of boot received.

*The $750,000 of additional depreciation deductions generated from the cost segregation study can be utilized to offset the entire $350,000 of taxable gain for 2022 because of the cash boot received. Note the remaining $400,000 of depreciation deductions are available to offset other taxable income for 2022.

Scenario #2. Outside the Bonus Depreciation Window: When bonus depreciation phases down after 2022, it becomes more difficult to generate year 1 deductions by performing a cost segregation study on the replacement property. In this case, it becomes more critical to consider a cost segregation on the relinquished property using a lookback cost segregation study.

In a look-back study, a cost-segregation specialist determines the cost allocation to the various property component categories as of the date the property was acquired. To capture the missed deductions created by a cost segregation study on the relinquished property that was placed in service in a prior year, an Automatic Change in Accounting Method (“Form 3115-DCN #7”) and a Section 481(a) adjustment is calculated in the year the cost segregation study is implemented (in our example below, 2021). The Section 481(a) adjustment from a study performed on a property that is to be exchanged in a 1031 transaction can offset taxable boot from the exchange[1].

KBKG Insight:

In order to use this strategy, Accounting Method rules require the taxpayer to own the relinquished property as of the first day of the year of change. As such, this strategy can only be used in the tax year the relinquished property is sold.

To understand how a cost segregation study performed on the relinquished property can help where cash boot was received, here is the following case study.

KBKG Case Study No Bonus:

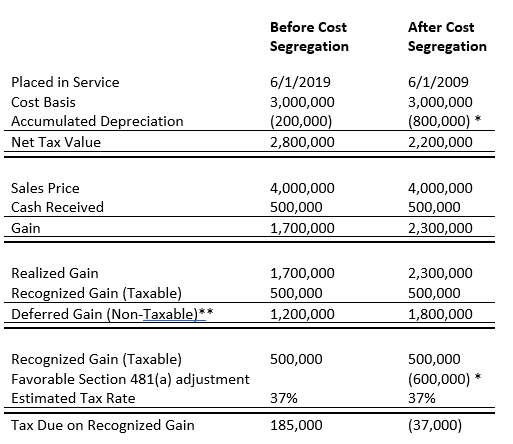

In 2019, Taxpayer A acquired a commercial building (less land) for $3,000,000 and depreciated the basis over 39 years for tax purposes. In 2021, Taxpayer A sold the property in a 1031 exchange for $4,000,000 + $500,000 of cash. The recognition of cash “boot” triggers a taxable event for Taxpayer A.

To offset the taxable gain on the cash boot received, Taxpayer A performed a cost segregation study and accelerated $600,000 of depreciation deductions utilizing Section 481(a) adjustment filed with an Automatic Accounting Method Change (“Form 3115 – DCN #7”) with the timely filed 2021 Tax Return. As a result, the entire gain of $500,000 was offset utilizing the additional deductions and Taxpayer A secured cash tax savings of $185,000 in 2021 by performing a cost segregation study.

Note the accelerated depreciation deductions does increase the deferred gain, which will reduce the basis of the replacement property in a 1031 exchange.

*Includes Section 481(a) adjustment from performing cost segregation

**Deferred Gain will reduce the basis of replacement property in 1031 exchange

KBKG Insight:

Based on the final and proposed 1031 regulations, relinquished property that is sold should be matched with replacement property that is received to determine gain; it is recommended to perform a cost segregation analysis on the replacement property if a cost segregation study was performed on the relinquished property to ensure all classes of property are matched to avoid recognizing gain on any unmatched property. For more information on 1031 matching issues, see our article on the Final Sec. 1031 Regulations published Feb. 4, 2021.

Conclusion

Cost segregation in conjunction with a 1031 exchange is a powerful tool, as long as the taxpayer and their advisor are familiar with the interaction of these tax laws. By performing a cost segregation study, taxpayers may be able to offset most, if not all the recognized gain attributable to the receipt of “boot” in a 1031 exchange. For CPA’s and tax preparers, using this sophisticated strategy to help clients pull tax free cash out of a 1031 exchange is the type of value-add consulting that can earn you a loyal client for years to come.

[1] KBKG Section 481(a) Calculator: https://www.kbkg.com/481a-calculator

About the Author

Amar Patel – Director

Southeast

Amar spent 15 years at a Big Four accounting firm and one year at Centiv, LLC, focusing on various specialty tax products including Cost Recovery Solutions and Research & Development Tax Credits. In the past 16 years of practice, Amar has become an expert in cost segregation and large fixed asset depreciation reviews for purposes of identifying federal, state, and property tax benefits. » Full Bio

Gian Pazzia – CEO

Pasadena

Gian P. Pazzia is currently CEO of KBKG and oversees all strategic initiatives for the company. He has over 20 years of experience in the specialty tax industry. He is a recognized leader in the cost segregation field serving as a former President (2013-2015 term) of the American Society of Cost Segregation Professionals (www.ASCSP.org) and held a seat on their Board of Directors for a decade. » Full Bio

Malik Javed – Principal

Pasadena

Malik S. Javed is a Principal and oversees engineering operations for Cost Segregation projects at KBKG. He is a Certified member of the American Society of Cost Segregation Professionals (ASCSP) and is currently a member of the ASCSP Technical Standards Committee. Since joining KBKG in 2004, Malik S. Javed has performed thousands of Cost Segregation studies for clients in various industries, regularly reviewed architectural and engineering drawings and construction cost budgets. » Full Bio