Each year, tax professionals who deal with real estate must evaluate the most recent building expenditures and determine which items should be written off as a repair expense or capitalized. The most common, and often significant, item that is evaluated is roofing-related work. In many cases, only a portion of the roofing system is replaced, and depending on the facts, those costs may be deducted as repairs. When compared to the alternative option of depreciating the cost over a 27.5-year life for residential rental real estate or a 39-year life for commercial real estate under the modified accelerated cost recovery system, an incorrect conclusion may lead to a significant overpayment of tax liability.

KBKG Insight: For the tax professional who has only cryptic invoice descriptions and no direct knowledge of the roof work, assembling the facts and circumstances can be a challenge. The key to properly evaluating the character and nature of the work performed is having a basic understanding of roofing systems and asking insightful questions.

KBKG’s Guide to Expensing Roofing Costs provides tax preparers an outline of which questions to ask clients and includes pictures and charts to reference when evaluating roof repair costs. Inside, our engineering experts bridge the gap between the scope of roofing work that was performed and rules set forth in the tangible property “repair” regulations (IRB 2013-43).

Analysis

A capital improvement is defined as an amount paid after a property is placed in service that results in a betterment, adaptation, or restoration to the unit of property or building system (Regs. Sec. 1.263(a)-3(d)). Replacing a substantial portion of any major component of a building meets the criteria of a capital improvement. A roof system is a major component because it performs a discrete and critical function in a building structure.

A roof system includes a roof structure and multiple layers of materials above it. The roof structure usually includes some type of deck spanning a network of load-bearing structural joists and beams. These load-bearing roof elements are less likely to be replaced unless a catastrophic failure occurs such as from a tornado or fire or long-term neglect of the roof cover. Our analysis will focus on the components above the load-bearing structural elements.

Step 1. What type of roof it is it?

When evaluating this issue, it’s important to have a basic knowledge of the physical characteristics of common roof systems. Roof systems are generally divided into two generic classifications: steep pitch and low pitch.

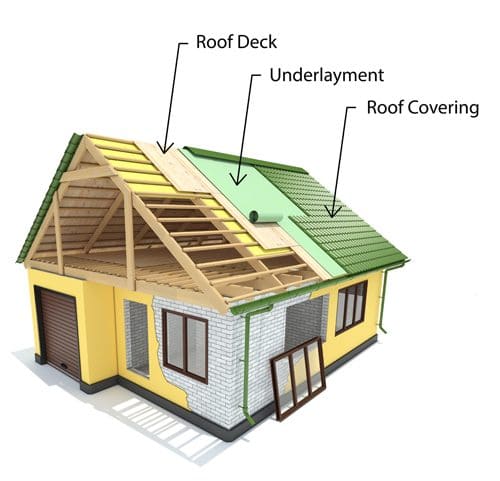

Steep-Pitch Roofing

Steep-pitch roof assemblies (typically used for residential rental properties) usually consist of three primary parts:

- Roof deck — the first layer above beams, usually a wood-based material similar to plywood and sometimes referred to as “sheathing.”

- Underlayment — provides a secondary weatherproofing barrier. Sometimes underlayment is referred to as “felt” or “paper.”

- Roof covering — can include various types of shingles, clay tile or concrete tile, slate, wood shakes, or metal roof systems for steep-pitch applications.

Generally, the average lifespan of steep pitch roofing covers is:

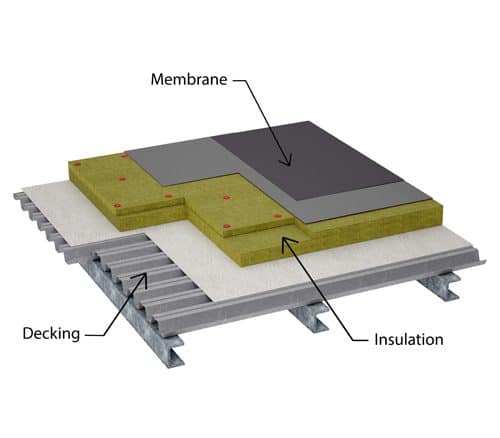

Low-Pitch or Flat Roofing

Most low-pitch roofing (typically used for commercial buildings) consists of three sections:

- Roof deck—typically a corrugated metal panel supported by structural beams.

- Insulation—one distinction from steep-pitch roofing is that insulation is typically above the decking and may be replaced with the membrane layer.

- Roof cover or membrane—most low pitch membranes or assemblies can be classified as built-up roof membranes, metal panel roof systems, modified bitumen sheet membranes, synthetic rubber membranes (e.g., EPDM), thermoplastic membranes (e.g., PVC, TPO), or spray polyurethane foam-based (SPF) roof systems.

Generally, the average lifespan of low pitch roofing covers is: